Table of Content

- Can I Lose My Home If I Don't Pay My HELOC?

- Rocket Mortgage

- Can a Home Equity Line Be Discharged in Bankruptcy?

- Borrowing Basics: Home Equity Loans vs. Cash Out

- Today's low home equity rates † Click to go to home equity assumptions page

- Home equity loan vs. line of credit? Here’s what you need to know

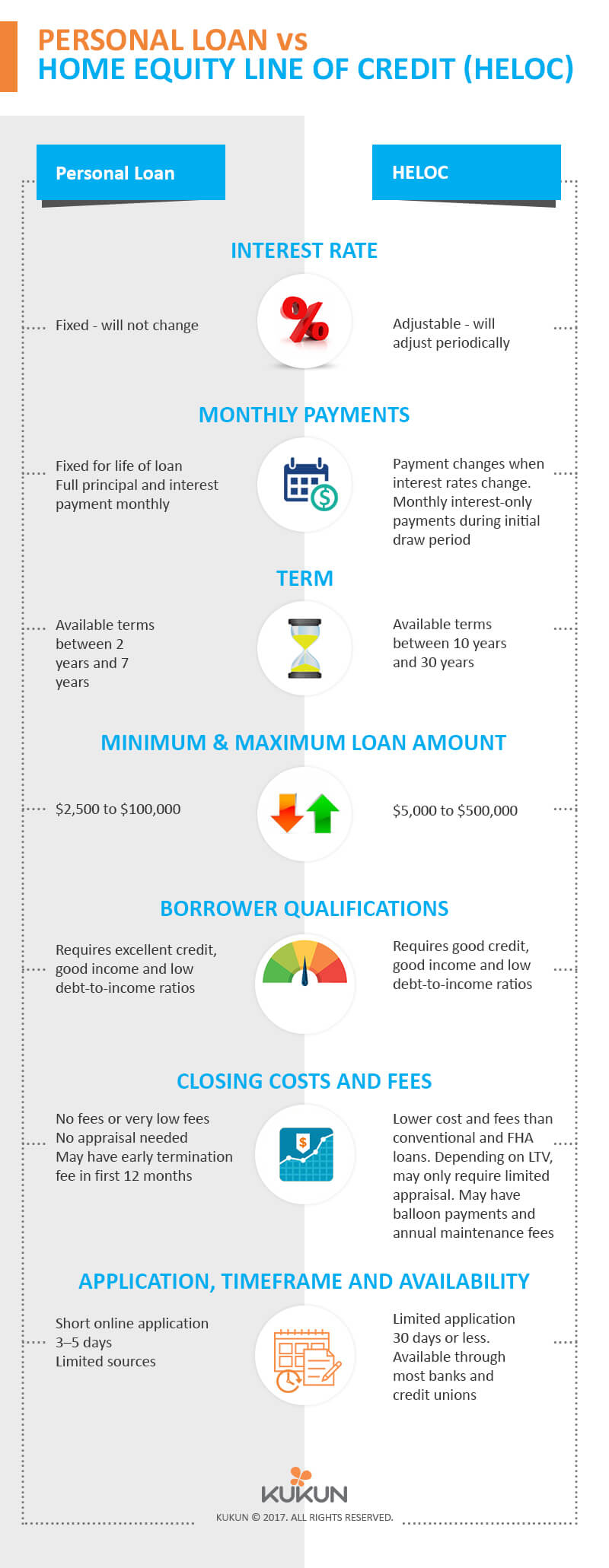

- What Is A Home Equity Line Of Credit?

With that in mind, I've decided to put an end to the confusion once and for all. It will cover what a home equity line of credit is, how it works, and how to qualify for one of your own. A monthly payment cannot be generated based upon the information provided. It helps you figure how much of a line of credit you can secure with your available home equity. A home equity loan calculator like this one takes that all into account to figure how just how much of a line of credit you may be able to obtain, depending on all those factors. The amount you can borrow with any home equity loan is determined by how much equity you have – that is, the current value of your home minus the balance owed on your mortgage.

The Difference Between Cash-Out Refinance And Home Equity Loan Refinancing - 4-minute read Patrick Chism - October 11, 2022 Cash-out refinance or home equity loan? Victoria Araj is a Section Editor for Rocket Mortgage and held roles in mortgage banking, public relations and more in her 15+ years with the company. She holds a bachelor’s degree in journalism with an emphasis in political science from Michigan State University, and a master’s degree in public administration from the University of Michigan. Keep in mind that your home is used as collateral for this type of loan, so if you’re unable to pay off the loans, you may lose your home as a consequence. Some people will use their home’s equity to pay for their own or their child’s college education.

Can I Lose My Home If I Don't Pay My HELOC?

You can use them to pay credit cards or other monthly expenses. Whether you are looking to purchase a new home or refinance your current mortgage, PHH Mortgage offers a wide variety of loan options, including conventional, VA and FHA. Talk with one of our experienced loan officers today to get started. You also can't be carrying too much debt – your total monthly debts, including your mortgage payments and all other loans, should not exceed 45 percent of your gross monthly income.

So if your home is worth $250,000 and you owe $150,000 on your mortgage, you have $100,000 in home equity. Want to calculate your payments for a home equity line of credit? Then use our Line of Credit Payments Calculator to figure your payments during the draw phase or our Home Equity Loan and HELOC Calculator to estimate payments over the entire loan.

Rocket Mortgage

Availing loans easily lead to overspending and stretches the borrower’s budget. HELOCs have various advantages and disadvantages, as described below. Borrowers can borrow 60-80% of the house equity for 30 years. Based on the information you have provided, you are eligible to continue your home loan process online with Rocket Mortgage.

HELOCs are also a form of secured debt, with the home acting as collateral. That means borrowers who default are at risk of losing their home. A home equity line of credit, also known as a HELOC, is a revolving line of credit that allows people to borrow against the equity in their homes. Home equity is the value a homeowner might build in their home over time. It’s defined by the difference between the current market value of a residence and what’s still owed on a mortgage. Mortgage products and services are offered through Truist Bank.

Can a Home Equity Line Be Discharged in Bankruptcy?

Let’s go back to our first example one more time, with your $250,000 home and $180,000 balance. With a cash-out refinance, you could borrow up to $200,000, use $180,000 of that to pay off your current mortgage and then keep the other $20,000 . There is technically no limit to how many HELOCs and home equity loans you have on the same property. Most lenders will allow a well-qualified borrower to access up to 85% of their home's equity through HELOCs and home equity loans.

The variable rate is calculated from both an index and a margin. You understand that you are not required to consent to receiving autodialed calls/texts as a condition of purchasing any Bank of America products or services. Any cellular/mobile telephone number you provide may incur charges from your mobile service provider. If you do not earn enough income and attempt to keep your home during bankruptcy, you could possibly face foreclosure after your bankruptcy and end up in a bad financial situation again. You will be required to pay some of it, but, generally, most Chapter 13 filers only end up paying a tiny fraction of the original debt back. Once the Chapter 13 is complete, the remainder of the HELOC debt will be discharged.

Remember, the $320,000 limit would include all existing loans secured by your home plus your new HELOC. Other private lenders—such as Sallie Mae, which offers student loans—work with a borrower who is struggling to meet payments by offering multiple deferments and forbearance options. There are two types of debt instruments used to turn the equity in your home into available cash. The first is a home equity loan , which is a set amount of money financed for a set period at a fixed interest rate and with a fixed payment.

There may also be opportunities to renew the line of credit. A home equity loan is similar to a HELOC in that it is a loan that is offered by a lender based on your home equity. Unlike HELOCs, you are unable to add on loan funds to your home equity loan, so it’s ideal if you know how much funding you need to the dollar. They may then continue this cycle as long as their home's value continues to rise. During the financial crisis when home values plummeted, many borrowers who used this method found their homes in foreclosure.

If you can't afford to pay your HELOC back, you may be at risk of losing your home to foreclosure. Doretha Clemons, Ph.D., MBA, PMP, has been a corporate IT executive and professor for 34 years. She is an adjunct professor at Connecticut State Colleges & Universities, Maryville University, and Indiana Wesleyan University. She is a Real Estate Investor and principal at Bruised Reed Housing Real Estate Trust, and a State of Connecticut Home Improvement License holder. And be sure to inquire about all the ways we can assist you with rate discounts.

I am blessed have had the Sunday episode with my vehicle which steered me towards Allmand Law Firm while searching for legal representation. Hopefully, I can get on with my life, rebound into a lifestyle that is comfortable, and with financial certainty. In cases where your outstanding debt on your first mortgage is very close to the value of your property, they may require a second appraisal before moving forward. Judges can be prickly about stripping liens off of property when the borrower consented to the lien. If you’ve used up the cash in your emergency fund, you could draw on a HELOC to pay for house repairs, medical bills or other unexpected costs.

The chart with the three colored lines shows you how your available line of credit would vary across a range of appraised home values, given the figures you entered into the calculator. The lines correspond to the loan-to-value ratio your lender will allow. To use it, enter the estimated value of your home, the amount owed on your mortgage and any second liens, and the maximum loan-to-value ratio allowed by your lender in the boxes indicated. The line of credit available to you will be displayed in the blue box at the top.

The key in all options is to get help right away instead of hoping the problem will disappear on its own. Many lenders will work with you if you're struggling to make payments, such as modifying the loan, but it's important to contact them as soon as possible. Borrowers can increase HELOC limits by applying for a loan modification. Or else going for a new HELOC by settling the current equity loan.

No comments:

Post a Comment